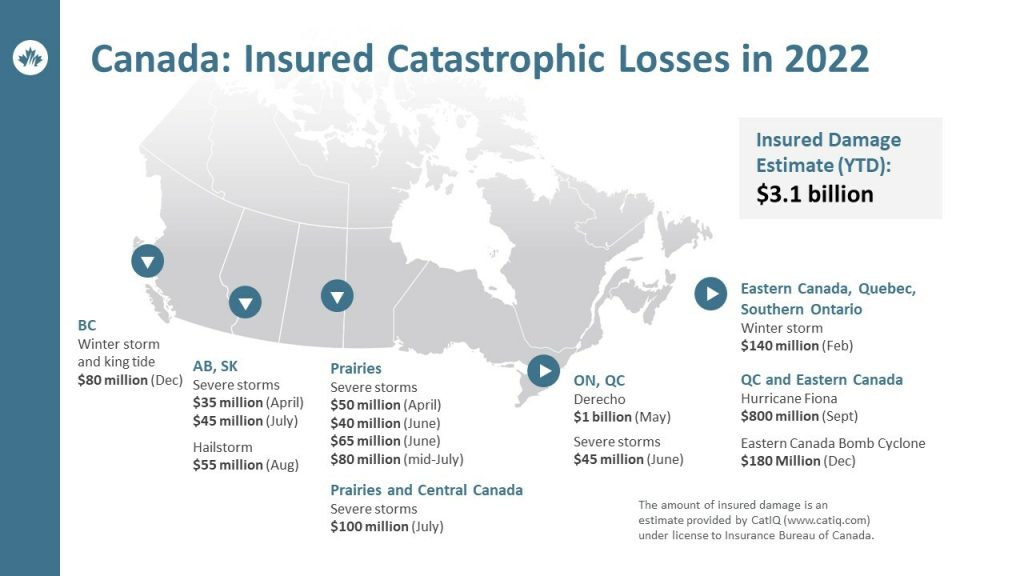

Severe weather across Canada continues to highlight the financial costs of a changing climate to insurers, governments and taxpayers. Nationally, insured damage for severe weather events reached $3.1 billion last year, according to Catastrophe Indices and Quantification Inc. (CatIQ).

2022 now ranks as the 3rd worst year for insured losses in Canadian history. While the $3.1 billion figure is alarming, no single catastrophic event nor any particular region accounted for the majority of losses. Unlike 2016, the highest loss year on record, where the Fort McMurray, Alberta, wildfire accounted for about 75% of national losses, 2022 saw disasters from nearly every part of the country.

Noteworthy severe weather events last year include Hurricane Fiona, the Ontario and Quebec derecho, the Eastern Canada late-winter storm, the Western Canada summer storms and the Eastern Canada bomb cyclone.

Insured Damage for Severe Weather Events in 2022

|

February 17–19 |

Eastern Canada late-winter storm |

$140 million |

|

April 22–25 |

Manitoba and Northwestern Ontario flooding |

$60 million |

|

May 21 |

$1 billion |

|

|

June 16–17 |

Ontario and Quebec severe storms |

$50 million |

|

July–August |

$300 million |

|

|

September 23–24 |

$800 million |

|

|

December 22–26 |

Eastern Canada bomb cyclone |

$180 million |

|

December 23–27 |

BC winter storm and king tide |

$80 million |

Canada’s Top 10 Highest Insured Loss Years on Record (loss and adjusted expenses in 2022 dollars)

|

Rank |

Year |

Total loss ($ billion) |

Notable severe weather event |

||

|

1 |

2016 |

5.96 |

Fort McMurray, Alberta, fire |

||

|

2 |

2013 |

3.87 |

Alberta floods; Greater Toronto Area (GTA) |

||

|

3 |

2022 |

3.12 |

Multiple events |

||

|

4 |

1998 |

2.83 |

Quebec ice storm |

||

|

5 |

2021 |

2.48 |

Calgary hailstorm; British Columbia floods |

||

|

6 |

2020 |

2.46 |

Fort McMurray, Alberta, flood; Calgary |

||

|

7 |

2018 |

2.40 |

Multiple events: Ontario and Quebec |

||

|

8 |

2011 |

1.97 |

Slave Lake, Alberta, fire and windstorm |

||

|

9 |

2012 |

1.65 |

Calgary rainstorm |

||

|

10 |

2019 |

1.56 |

Multiple events |

||

Sources 1983–2007: IBC, PCS Canada, Swiss Re, Deloitte. 2008–2021: CatIQ.

“Canada is increasingly a riskier place to live, work and insure,” said Craig Stewart, Vice-President, Climate Change and Federal Issues, Insurance Bureau of Canada (IBC). “Governments have spent far too little attention to adaptation in the discourse over climate policy. This spring, the federal government needs to lead the way in finalizing a National Adaptation Strategy and boldly funding both community-level infrastructure and property-level retrofits that increase resilience to floods, windstorms, heat events and wildfires.

“In particular, we’re seeing early signs that property insurance may become less affordable or even unavailable as global reinsurers shift capacity away from riskier countries,” continues Stewart. “Now is the time for Canadian insurers and governments to partner on a National Flood Insurance Program to ensure Canadian homeowners remain financially resilient in the face of these growing number and severity of events.”

IBC continues in-depth discussions with the federal and provincial governments on ways to improve the resilience of communities and better manage the costs of flooding for high-risk residential properties in Canada. Federal, provincial, territorial and Indigenous governments collaborated with insurers to finalize the “Task Force Report on Flood Insurance and Relocation” in August 2022. The federal government is now examining options to create a national residential flood insurance program that will offer affordable insurance to all residents at high risk of overland flooding, including storm surge, through a public-private partnership. Most G7 countries already have such a program in place.

In today’s world of extreme weather events, insured catastrophic losses in Canada now routinely exceed $2 billion annually, most of it due to water-related damage. In the decade before 2008, Canadian insurers averaged only $456 million a year in severe weather-related losses.